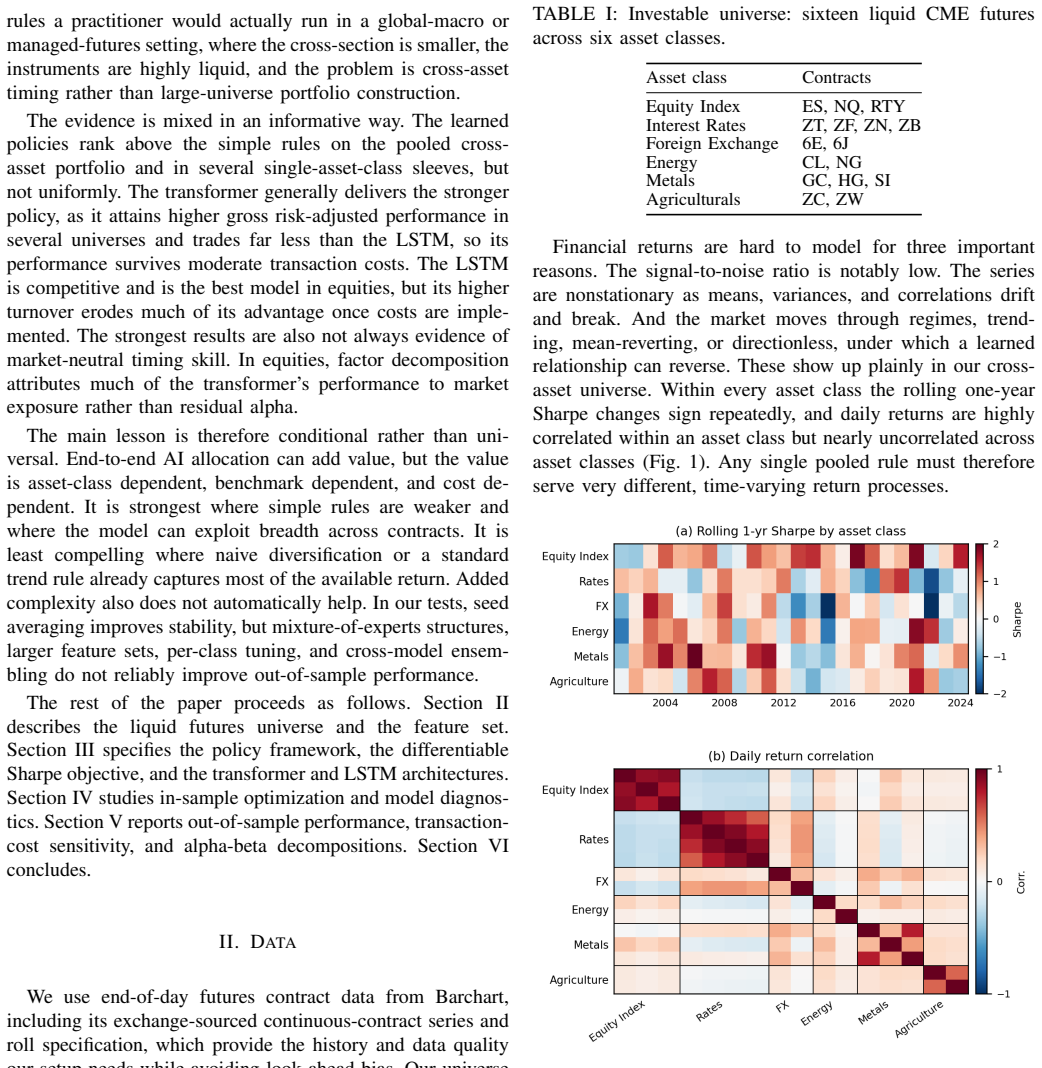

0

Trend profits collapsed on small-tick futures after 2008

Is Trend Still Your Friend?: A Microstructural Account of the Demise of Short-Term Trend-Following

The split by volatility-normalised tick size shows HFT liquidity withdrawal broke the impact loop that once sustained short-term trends.

full image

full image

abstract click to expand

Systematic trend following has, on average, been profitable for at least two centuries; yet since approximately 2009, short-term trends have ceased to deliver reliable returns. Using a cross-section of roughly 100 liquid futures contracts spanning 1995-2025, together with an industry-representative CTA proxy, we document the break and characterise its dependence on signal speed and asset class. We evaluate four candidate explanations - capacity constraints, market electronification, a regime change in CTA-versus-order-flow interactions, and a microstructural mechanism - and find that the first three fail on grounds of timing, magnitude, or cross-sectional heterogeneity.

Our central empirical finding is that the cross-sectional variable distinguishing degraded from surviving trends is the volatility-normalised tick size: post-2008 trend PnL has collapsed on small-tick contracts across all signal horizons, while remaining essentially intact on large-tick ones. Neither asset class nor liquidity replicates this dichotomy.

We interpret this result through a self-fulfilling feedback loop that, in our view, lies at the heart of the trend anomaly itself: trend signals trigger directional trades, whose market impact reinforces the very price moves that generated the signal. Both the profitability and the persistence of trend are sustained by this impact channel, which requires that trend followers can execute aggressively at reasonable cost. We argue that the post-crisis transition to HFT-dominated market making, whose liquidity-withdrawal behaviour in front of predictable directional flow has sharply contrasting consequences for sparse (small-tick) and dense (large-tick) limit order books, has broken this loop on small-tick contracts. On large-tick contracts, residual depth remains sufficient, and the loop continues to operate.