Enhancing a Risk Model by Adding Transient Statistical Factors

Pith reviewed 2026-06-30 21:24 UTC · model grok-4.3

The pith

An existing risk model is enhanced by adding new statistical factors recovered via maximum likelihood from historical returns.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The proposed extension refines the given factor model and adds new statistical factors estimated by maximum likelihood on the sequence of realized returns, and thereby captures structure in the returns that is missed by the original model.

What carries the argument

Maximum likelihood estimation on weighted historical returns to recover additional transient statistical factors, with explicit handling for missing data.

If this is right

- The enhanced model supplies a more complete decomposition of asset return variability into common and idiosyncratic components.

- Transient factors and changing market regimes become explicitly represented in the covariance estimates.

- The method remains applicable to equity datasets that contain missing returns.

- Third-party risk models can be systematically refined without requiring new external data sources.

Where Pith is reading between the lines

- Portfolio managers could apply the same procedure to any proprietary or vendor-supplied risk model to obtain updated covariance estimates.

- The half-life hyperparameter offers a direct way to control the time scale of the transient effects being extracted.

- Repeated application on rolling windows of returns would produce a sequence of evolving risk models.

Load-bearing premise

The additional factors recovered by maximum likelihood on historical returns represent genuine transient statistical structure rather than noise or overfitting artifacts induced by the choice of the two hyperparameters.

What would settle it

Out-of-sample log-likelihood on held-out returns fails to increase, or portfolio risk forecasts show no improvement, when the added factors are included versus the original model alone.

Figures

read the original abstract

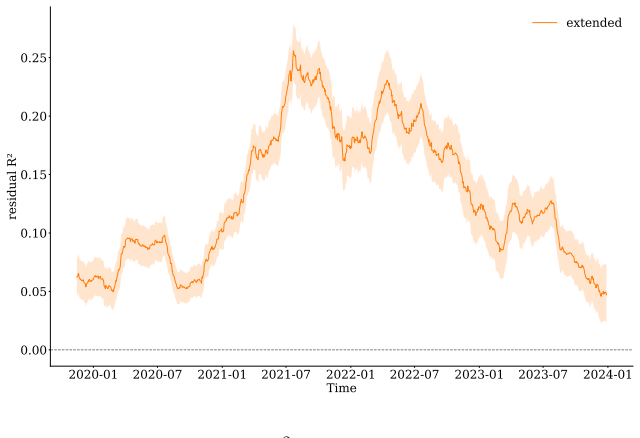

Estimating the covariance of asset returns, i.e., the risk model, is a key component of financial portfolio construction and evaluation. Most risk modeling approaches produce a factor model that decomposes the asset variability into two components: the first attributed to a small number of factors that are common among the assets and the second attributed to the idiosyncratic behavior of each asset. Third-party providers typically provide risk models to investors, and while these models are typically of high quality, they may fail to capture important information, e.g., changing market regimes and transient factors. To overcome these limitations, we propose a systematic method based on maximum likelihood estimation to enhance an existing factor model by both refining the given model and adding new statistical factors. Our approach relies only on the observed sequence of realized returns and on the choice of two hyperparameters: the number of additional factors and the half-life parameter that determines the weights assigned to returns in the log-likelihood objective. Importantly, our methodology applies to the situation where asset returns may be missing, making it suitable for typical equity datasets. We demonstrate our approach on the Barra short-term US risk model, a high-quality risk model used in practice, for a universe of US high-capitalization equities. We show that the proposed extension captures structure in the returns that is missed by the original model.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a maximum likelihood estimation method to enhance an existing factor risk model (e.g., Barra short-term US) by refining its factors and adding new transient statistical factors. The approach uses only the observed sequence of realized asset returns (accommodating missing values) and requires selection of two hyperparameters: the number of additional factors and a half-life parameter that weights returns in the log-likelihood. It is demonstrated on US high-capitalization equities, with the claim that the extension captures structure missed by the original model.

Significance. The method's ability to handle missing returns is a practical strength for equity datasets. If the added factors can be shown to reflect genuine transient covariance rather than artifacts, the approach could offer a systematic way to augment commercial risk models. However, the current presentation provides no quantitative evidence of improvement, limiting immediate significance.

major comments (2)

- [Abstract] Abstract: The claim that 'the proposed extension captures structure in the returns that is missed by the original model' is presented without any quantitative metrics (e.g., likelihood ratios, out-of-sample covariance errors, or portfolio performance deltas), out-of-sample tests, or baseline comparisons, preventing assessment of whether reported gains exceed what would be expected from fitting noise.

- [Demonstration section] Demonstration on Barra model: The additional factors and refinements are obtained by MLE directly on the same historical returns sequence used for evaluation, with both the number of factors and half-life chosen from this data; no held-out periods, cross-validation, or null simulations are indicated to distinguish transient structure from overfitting induced by the two free hyperparameters.

minor comments (1)

- [Abstract] The abstract would be strengthened by including at least one concrete quantitative result from the demonstration (e.g., a reported improvement in log-likelihood or risk metric).

Simulated Author's Rebuttal

We thank the referee for their constructive comments on the need for stronger quantitative validation. We address each major comment below.

read point-by-point responses

-

Referee: [Abstract] Abstract: The claim that 'the proposed extension captures structure in the returns that is missed by the original model' is presented without any quantitative metrics (e.g., likelihood ratios, out-of-sample covariance errors, or portfolio performance deltas), out-of-sample tests, or baseline comparisons, preventing assessment of whether reported gains exceed what would be expected from fitting noise.

Authors: The demonstration section compares log-likelihoods between the original and enhanced models on the observed returns. We agree the abstract claim would be strengthened by explicit metrics. In revision we will update the abstract to reference these likelihood improvements and add out-of-sample covariance errors, likelihood-ratio tests, and baseline comparisons. revision: yes

-

Referee: [Demonstration section] Demonstration on Barra model: The additional factors and refinements are obtained by MLE directly on the same historical returns sequence used for evaluation, with both the number of factors and half-life chosen from this data; no held-out periods, cross-validation, or null simulations are indicated to distinguish transient structure from overfitting induced by the two free hyperparameters.

Authors: We agree that in-sample hyperparameter selection on the same returns sequence leaves open the possibility of overfitting. The method is designed to operate on observed returns, but to address this we will add cross-validation for selecting the number of factors and half-life, plus null simulations on randomized returns, in the revised manuscript. revision: yes

Circularity Check

No significant circularity in derivation chain

full rationale

The paper proposes an MLE-based procedure to refine an existing factor model and add transient factors, with the procedure explicitly depending on observed returns plus two user-chosen hyperparameters. The demonstration consists of applying this fitting procedure to the Barra short-term model on a panel of US equity returns. No step in the provided text reduces a claimed prediction or first-principles result to its own inputs by construction; the method is a standard likelihood maximization whose output is the fitted factors themselves. No self-citation chains, uniqueness theorems, or smuggled ansatzes are invoked as load-bearing. The central empirical claim is therefore an application of the stated procedure rather than a tautological renaming or self-referential derivation.

Axiom & Free-Parameter Ledger

free parameters (2)

- number of additional factors

- half-life parameter

axioms (2)

- domain assumption Asset returns follow a multivariate normal distribution conditional on the factors.

- domain assumption The original Barra factor loadings and variances are treated as fixed inputs that can be refined.

Reference graph

Works this paper leans on

-

[1]

Large Dimensional Factor Analysis.Foundations and Trends® in Econometrics, 3(2):89–163, 2008

Jushan Bai and Serena Ng. Large Dimensional Factor Analysis.Foundations and Trends® in Econometrics, 3(2):89–163, 2008

2008

-

[2]

Markowitz Portfolio Construction at Seventy.Journal of Portfolio Management, 50(8):117– 160, 2024

Stephen Boyd, Kasper Johansson, Ronald Kahn, Philipp Schiele, and Thomas Schmelzer. Markowitz Portfolio Construction at Seventy.Journal of Portfolio Management, 50(8):117– 160, 2024

2024

-

[3]

Thematic Investing: A Risk-Based Perspective.Financial Analysts Journal, 81(4):103– 120, 2025

Emmanuel Cand` es, Trevor Hastie, Ked Hogan, Ronald N Kahn, Robert Luo, and Asher Spec- tor. Thematic Investing: A Risk-Based Perspective.Financial Analysts Journal, 81(4):103– 120, 2025

2025

-

[4]

Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation.Econometrica: Journal of the Econometric Society, pages 987– 1007, 1982

Robert F Engle. Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation.Econometrica: Journal of the Econometric Society, pages 987– 1007, 1982

1982

-

[5]

Wiley, 2008

Frank J Fabozzi.Handbook of Finance, Investment Management and Financial Management, volume 2. Wiley, 2008

2008

-

[6]

The Cross-Section of Expected Stock Returns.The Journal of Finance, 47(2):427–465, 1992

Eugene F Fama and Kenneth R French. The Cross-Section of Expected Stock Returns.The Journal of Finance, 47(2):427–465, 1992

1992

-

[7]

Common Risk Factors in the Returns on Stocks and Bonds.Journal of Financial Economics, 33(1):3–56, 1993

Eugene F Fama and Kenneth R French. Common Risk Factors in the Returns on Stocks and Bonds.Journal of Financial Economics, 33(1):3–56, 1993

1993

-

[8]

High Dimensional Covariance Matrix Estimation using a Factor Model.Journal of Econometrics, 147(1):186–197, 2008

Jianqing Fan, Yingying Fan, and Jinchi Lv. High Dimensional Covariance Matrix Estimation using a Factor Model.Journal of Econometrics, 147(1):186–197, 2008

2008

-

[9]

An Overview of the Estimation of Large Covariance and Precision Matrices.The Econometrics Journal, 19(1):C1–C32, 2016

Jianqing Fan, Yuan Liao, and Han Liu. An Overview of the Estimation of Large Covariance and Precision Matrices.The Econometrics Journal, 19(1):C1–C32, 2016

2016

-

[10]

McGraw Hill New York, 2000

Richard C Grinold and Ronald N Kahn.Active Portfolio Management. McGraw Hill New York, 2000

2000

-

[11]

Springer, 2nd edition, 2009

Trevor Hastie, Robert Tibshirani, and Jerome Friedman.The Elements of Statistical Learning. Springer, 2nd edition, 2009

2009

-

[12]

A Simple Method for Predicting Covariance Matrices of Financial Returns.Foundations and Trends®in Econometrics, 12(4):324–407, 2023

Kasper Johansson, Mehmet G Ogut, Markus Pelger, Thomas Schmelzer, and Stephen Boyd. A Simple Method for Predicting Covariance Matrices of Financial Returns.Foundations and Trends®in Econometrics, 12(4):324–407, 2023

2023

-

[13]

Riskmetrics–Technical Document, 1996

REUTERS JP Morgan. Riskmetrics–Technical Document, 1996

1996

-

[14]

Honey, I Shrunk the Sample Covariance Matrix.The Journal of Portfolio Management, 30(4):110–119, 2004

Olivier Ledoit and Michael Wolf. Honey, I Shrunk the Sample Covariance Matrix.The Journal of Portfolio Management, 30(4):110–119, 2004

2004

-

[15]

Narrative Factors and Risk Models.Available at SSRN 5271271, 2025

Wai Lee, Ryan Brown, and Harin de Silva. Narrative Factors and Risk Models.Available at SSRN 5271271, 2025

2025

-

[16]

K. V. Mardia, J. T. Kent, and J. M. Bibby.Multivariate Analysis. Academic Press, 1979

1979

-

[17]

Portfolio Selection.The Journal of Finance, 7(1):77–91, 1952

Harry Markowitz. Portfolio Selection.The Journal of Finance, 7(1):77–91, 1952. 31

1952

-

[18]

Princeton University Press, 2015

Alexander J McNeil, R¨ udiger Frey, and Paul Embrechts.Quantitative Risk Management: Concepts, Techniques and Tools-Revised Edition. Princeton University Press, 2015

2015

-

[19]

The Barra US Equity Model (USE4), Methodology Notes.MSCI Barra, 2011

Jose Menchero, D Orr, and Jun Wang. The Barra US Equity Model (USE4), Methodology Notes.MSCI Barra, 2011

2011

-

[20]

Custom Factor Attribution.Financial Analysts Journal, 64(2):81–92, 2008

Jose Menchero and Vijay Poduri. Custom Factor Attribution.Financial Analysts Journal, 64(2):81–92, 2008

2008

-

[21]

MSCI Barra Risk Models.https://app2.msci.com/products/analytics/ models/

MSCI Inc. MSCI Barra Risk Models.https://app2.msci.com/products/analytics/ models/

-

[22]

The Fundamentals of Fundamental Factor Models.MSCI Barra Research Paper, (2010-24), 2010

Frank Nielsen and Jennifer Bender. The Fundamentals of Fundamental Factor Models.MSCI Barra Research Paper, (2010-24), 2010

2010

-

[23]

Noisy Covariance Matrices and Portfolio Optimization II

Szil´ ard Pafka and Imre Kondor. Noisy Covariance Matrices and Portfolio Optimization II. Physica A: Statistical Mechanics and its Applications, 319:487–494, 2003

2003

-

[24]

Extra-Market Components of Covariance in Security Returns.Journal of Financial and quantitative analysis, 9(2):263–274, 1974

Barr Rosenberg. Extra-Market Components of Covariance in Security Returns.Journal of Financial and quantitative analysis, 9(2):263–274, 1974

1974

-

[25]

EM Algorithms for ML Factor Analysis.Psychome- trika, 47(1):69–76, 1982

Donald B Rubin and Dorothy T Thayer. EM Algorithms for ML Factor Analysis.Psychome- trika, 47(1):69–76, 1982

1982

-

[26]

An Iterative Projections Algorithm for ML Factor Analysis

Abd-Krim Seghouane. An Iterative Projections Algorithm for ML Factor Analysis. InIEEE Workshop on Machine Learning for Signal Processing, pages 333–338, 2008

2008

-

[27]

Capital Asset Prices: A Theory of Market Equilibrium under Conditions of Risk.The Journal of Finance, 19(3):425–442, 1964

William F Sharpe. Capital Asset Prices: A Theory of Market Equilibrium under Conditions of Risk.The Journal of Finance, 19(3):425–442, 1964

1964

-

[28]

Asher Spector, Rina Foygel Barber, Trevor Hastie, Ronald N Kahn, and Emmanuel Cand` es. The Mosaic Permutation Test: An Exact and Nonparametric Goodness-of-Fit Test for Factor Models.arXiv preprint arXiv:2404.15017, 2024

-

[29]

Nonstationarities in Stock Returns.Review of Economics and Statistics, 87(3):503–522, 2005

C˘ at˘ alin St˘ aric˘ a and Clive Granger. Nonstationarities in Stock Returns.Review of Economics and Statistics, 87(3):503–522, 2005

2005

-

[30]

Kingsley Yeon and Mihai Anitescu. Beyond Low Rank: Fast Low-Rank + Diagonal Decom- position with a Spectral Approach.arXiv preprint arXiv:2512.17120, 2025. 32

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.