Avellaneda-Stoikov and Cartea-Jaimungal as One Framework: A Forced Uniqueness Theorem for Inventory Market Making

Pith reviewed 2026-06-28 15:36 UTC · model grok-4.3

The pith

Axioms on dynamic preferences force the Avellaneda-Stoikov and Cartea-Jaimungal market-making frameworks to be two views of the same entropic object with linked parameters.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

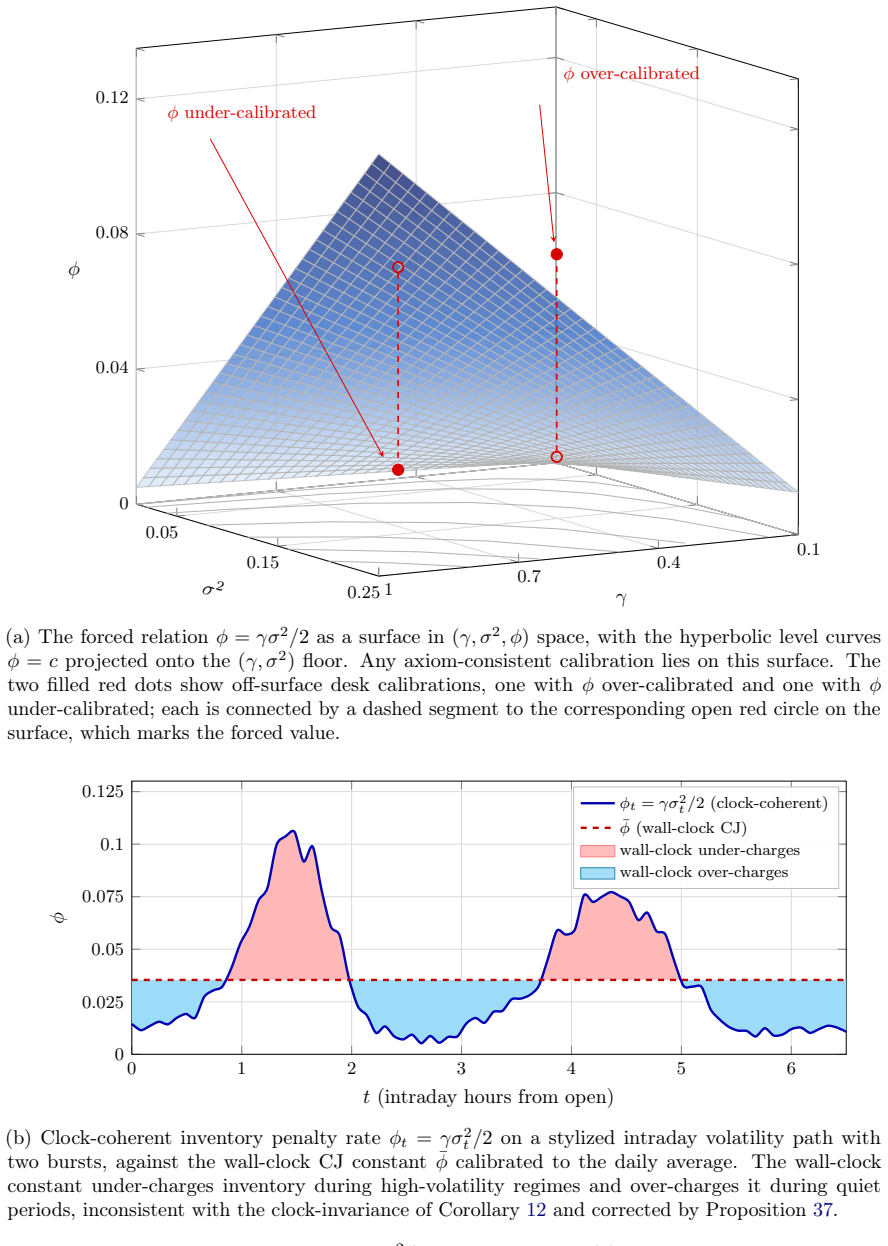

Under the five listed axioms the preference functional is forced to be the entropic certainty-equivalent on liquidation-adjusted terminal wealth parametrized by a single positive scalar γ; the Avellaneda-Stoikov framework is therefore the unique model in this class, while the Cartea-Jaimungal framework is its second-order Taylor expansion in inventory magnitude with the running coefficient forced to φ = γ σ² / 2 and the terminal coefficient forced to α = ½ L''(0) under the stated regularity condition on the liquidation cost.

What carries the argument

The entropic certainty-equivalent on liquidation-adjusted terminal wealth, parametrized by a single positive scalar γ, which encodes the entire preference structure.

If this is right

- The two frameworks cannot be treated as competing alternatives whose choice is driven only by tractability; they are different manifestations of one preference object.

- The relation γ = 2 φ / σ² supplies an immediate consistency cross-check on any pair of independently calibrated desk parameters.

- Higher-order expansions of the same entropic functional would generate further market-making approximations whose coefficients are likewise determined by the single scalar γ.

- Any model that preserves the five axioms must reproduce the same entropic form and therefore the same parameter linkage.

Where Pith is reading between the lines

- If the relation is observed to hold in practice, it would suggest that real market-maker risk preferences are close to entropic on liquidation-adjusted wealth.

- The unification opens the possibility of importing approximation techniques or numerical methods from one literature directly into the other without re-calibrating free parameters.

- Extensions to multi-asset or stochastic-volatility settings could be tested for consistency by checking whether the same γ continues to link the running and terminal penalties across assets.

Load-bearing premise

The mild regularity condition on the liquidation cost function that is used to force the terminal coefficient α to equal ½ L''(0).

What would settle it

Independent calibration of both frameworks on identical market data, followed by a direct check whether the fitted values satisfy φ = γ σ² / 2 within statistical error; systematic violation on multiple assets or periods would falsify the forced uniqueness.

Figures

read the original abstract

In inventory market making, the running-penalty coefficient $\phi$ of the Cartea-Jaimungal framework and the risk-aversion parameter $\gamma$ of the Avellaneda-Stoikov framework are typically treated as independent free parameters, calibrated separately. We show that they are in fact not independent. A small set of axioms on the market maker's dynamic preference functional, namely cash-additivity, normalization, concavity, strong dynamic consistency, and law-invariance, forces the preference functional to be the entropic certainty-equivalent on liquidation-adjusted terminal wealth, parametrized by a single positive scalar $\gamma$. The Avellaneda-Stoikov framework is the unique representative of this axiom class. The Cartea-Jaimungal framework is its second-order Taylor expansion in inventory magnitude, with the running coefficient forced to $\phi = \gamma\sigma^2/2$ and (under a mild regularity condition on the liquidation cost) the terminal coefficient forced to $\alpha = \frac{1}{2}L''(0)$. The two frameworks, typically presented as competing alternatives with the choice between them driven by tractability, are different manifestations of a single underlying object. The forced relation is invertible, $\gamma = 2\phi/\sigma^2$, giving a consistency cross-check on independently calibrated desk parameters.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims that five axioms on the market maker's dynamic preference functional (cash-additivity, normalization, concavity, strong dynamic consistency, and law-invariance) force the functional to be the entropic certainty-equivalent on liquidation-adjusted terminal wealth, parametrized by a single positive scalar γ. The Avellaneda-Stoikov framework is the unique representative of this axiom class. The Cartea-Jaimungal framework is its second-order Taylor expansion in inventory magnitude, with the running coefficient forced to φ = γσ²/2 and (under a mild regularity condition on the liquidation cost function) the terminal coefficient forced to α = ½L''(0). The forced relation is invertible, γ = 2φ/σ², providing a consistency cross-check on independently calibrated parameters.

Significance. If the result holds, the paper unifies two standard inventory market-making frameworks by deriving them from the same axiomatic preference structure, showing they are manifestations of a single object rather than competing alternatives. This supplies a theoretical basis for relating their free parameters and a practical cross-check on desk calibrations. The axiomatic derivation yielding a parameter-free uniqueness result and the explicit invertible relation between γ and φ are strengths that would be valuable to the mathematical finance literature on market making.

major comments (2)

- [Abstract (Taylor expansion paragraph)] Abstract, paragraph on the Taylor expansion: The relation α = ½ L''(0) is qualified by a 'mild regularity condition on the liquidation cost function.' The manuscript must explicitly define this condition (e.g., twice differentiability of L at zero and isolation of the second-derivative term) and state the consequences if it fails, because the uniqueness theorem itself does not invoke the condition; without it the terminal penalty in the Cartea-Jaimungal approximation is no longer pinned by the same γ, so the 'single underlying object' claim holds only for the running penalty φ.

- [Uniqueness theorem derivation] Derivation of the entropic form (section containing the uniqueness theorem): The abstract asserts that the five axioms force the entropic certainty-equivalent. The full proof steps from strong dynamic consistency and law-invariance to this specific functional form must be checked to confirm that the subsequent Taylor-expansion step does not introduce post-hoc restrictions that affect the central claim relating the two frameworks.

Simulated Author's Rebuttal

We thank the referee for the detailed and constructive report. The comments highlight important points on clarity and the precise scope of the uniqueness result versus its approximation. We address each major comment below and indicate the revisions we will make.

read point-by-point responses

-

Referee: [Abstract (Taylor expansion paragraph)] Abstract, paragraph on the Taylor expansion: The relation α = ½ L''(0) is qualified by a 'mild regularity condition on the liquidation cost function.' The manuscript must explicitly define this condition (e.g., twice differentiability of L at zero and isolation of the second-derivative term) and state the consequences if it fails, because the uniqueness theorem itself does not invoke the condition; without it the terminal penalty in the Cartea-Jaimungal approximation is no longer pinned by the same γ, so the 'single underlying object' claim holds only for the running penalty φ.

Authors: We agree that the mild regularity condition requires explicit definition and that its failure affects only the terminal coefficient. We will revise the abstract and the relevant section on the Taylor expansion to state the condition as twice continuous differentiability of the liquidation cost L at zero (with the second-derivative term isolated after the first-order term vanishes by normalization). If the condition fails, the terminal penalty α in the Cartea-Jaimungal approximation is no longer forced to equal ½L''(0) by the same γ, while the running-penalty relation φ = γσ²/2 continues to hold unconditionally from the second-order expansion of the entropic functional. The uniqueness theorem itself remains unaffected, as it concerns only the entropic form; the 'single underlying object' claim will be qualified accordingly in the revised text. revision: yes

-

Referee: [Uniqueness theorem derivation] Derivation of the entropic form (section containing the uniqueness theorem): The abstract asserts that the five axioms force the entropic certainty-equivalent. The full proof steps from strong dynamic consistency and law-invariance to this specific functional form must be checked to confirm that the subsequent Taylor-expansion step does not introduce post-hoc restrictions that affect the central claim relating the two frameworks.

Authors: The uniqueness theorem is proved in Section 3. The argument proceeds by first invoking cash-additivity, normalization and concavity to obtain a concave monetary utility functional, then applying strong dynamic consistency to obtain a recursive representation, and finally using law-invariance to reduce the problem to a static entropic form on the terminal liquidation-adjusted wealth; the resulting functional is necessarily the entropic certainty equivalent parametrized by a single γ > 0. The Taylor-expansion step that produces the Cartea-Jaimungal running and terminal penalties is applied only after the uniqueness result has been established and does not feed back into the axiomatic derivation. Consequently, no post-hoc restrictions are introduced. We are prepared to expand the proof steps in an appendix if the editor requests further detail, but the existing derivation already separates the axiomatic uniqueness from the subsequent approximation. revision: no

Circularity Check

Derivation from external axioms to entropic form and Taylor relations is self-contained with no reduction by construction.

full rationale

The paper states a list of axioms (cash-additivity, normalization, concavity, strong dynamic consistency, law-invariance) and claims they force the preference functional to be the entropic certainty-equivalent parametrized by γ; the AS framework is declared the unique representative and CJ its second-order expansion with φ = γσ²/2 and α = ½L''(0) under a regularity condition. No step reduces to a self-definition, a fitted input relabeled as prediction, or a load-bearing self-citation whose content is itself unverified. The uniqueness theorem and expansion are presented as derived within the paper rather than imported from overlapping prior work by the same author. The regularity condition is an explicit additional assumption, not a hidden tautology. The central claim therefore retains independent content relative to its inputs.

Axiom & Free-Parameter Ledger

free parameters (1)

- γ

axioms (5)

- domain assumption cash-additivity

- domain assumption normalization

- domain assumption concavity

- domain assumption strong dynamic consistency

- domain assumption law-invariance

Forward citations

Cited by 1 Pith paper

-

Axiomatic Market Making

Eight axioms force a unique three-parameter quoting rule for market makers with linear mid-quote in inventory and additive spread components.

Reference graph

Works this paper leans on

-

[1]

Efficient Market Making via Convex Optimization, and a Connection to Online Learning

Abernethy, J., Y.\ Chen, and J.\ W.\ Vaughan (2013). Efficient Market Making via Convex Optimization, and a Connection to Online Learning. ACM Transactions on Economics and Computation 1(2), 12:1--12:39

2013

-

[2]

On Risk Measures, Market Making, and Exponential Families

Abernethy, J., R.\ Frongillo, and S.\ Kutty (2014). On Risk Measures, Market Making, and Exponential Families. ACM SIGecom Exchanges 13(2), 21--25

2014

-

[3]

Dynamic Risk Measures

Acciaio, B.\ and I.\ Penner (2011). Dynamic Risk Measures. In Advanced Mathematical Methods for Finance, pp.\ 1--34. Springer

2011

-

[4]

Optimal Execution of Portfolio Transactions

Almgren, R.\ and N.\ Chriss (2000). Optimal Execution of Portfolio Transactions. Journal of Risk 3(2), 5--40

2000

-

[5]

Order Flow, Transaction Clock, and Normality of Asset Returns

An\'e, T.\ and H.\ Geman (2000). Order Flow, Transaction Clock, and Normality of Asset Returns. Journal of Finance 55(5), 2259--2284

2000

-

[6]

Coherent Measures of Risk

Artzner, P., F.\ Delbaen, J.-M.\ Eber, and D.\ Heath (1999). Coherent Measures of Risk. Mathematical Finance 9(3), 203--228

1999

-

[7]

Coherent multiperiod risk adjusted values and Bellman's principle

Artzner, P., F.\ Delbaen, J.-M.\ Eber, D.\ Heath, and H.\ Ku (2007). Coherent multiperiod risk adjusted values and Bellman's principle. Annals of Operations Research 152(1), 5--22

2007

-

[8]

High-frequency trading in a limit order book

Avellaneda, M.\ and S.\ Stoikov (2008). High-frequency trading in a limit order book. Quantitative Finance 8(3), 217--224

2008

-

[9]

The Nature of Price Returns During Periods of High Market Activity

Al Dayri, K., E.\ Bacry, and J.-F.\ Muzy (2011). The Nature of Price Returns During Periods of High Market Activity. In F.\ Abergel, B.\ K.\ Chakrabarti, A.\ Chakraborti, and M.\ Mitra (Eds.), Econophysics of Order-driven Markets, New Economic Windows, pp.\ 155--172. Springer, Milano

2011

-

[10]

Optimal Quoting under Adverse Selection and Price Reading

Barzykin, A., P.\ Bergault, O.\ Gu\'eant, and M.\ Lemmel (2025). Optimal Quoting under Adverse Selection and Price Reading. arXiv preprint arXiv:2508.20225

work page internal anchor Pith review Pith/arXiv arXiv 2025

-

[11]

Dynamic Mean-Variance Asset Allocation

Basak, S.\ and G.\ Chabakauri (2010). Dynamic Mean-Variance Asset Allocation. Review of Financial Studies 23(8), 2970--3016

2010

-

[12]

Minimum capital requirements for market risk

Basel Committee on Banking Supervision (2019). Minimum capital requirements for market risk. Bank for International Settlements, Basel, January 2019

2019

-

[13]

Time consistent dynamic risk processes

Bion-Nadal, J.\ (2009). Time consistent dynamic risk processes. Stochastic Processes and their Applications 119(2), 633--654

2009

-

[14]

A theory of Markovian time-inconsistent stochastic control in discrete time

Bj\"ork, T.\ and A.\ Murgoci (2014). A theory of Markovian time-inconsistent stochastic control in discrete time. Finance and Stochastics 18(3), 545--592

2014

-

[15]

Point Processes and Queues: Martingale Dynamics

Br\'emaud, P.\ (1981). Point Processes and Queues: Martingale Dynamics. Springer Series in Statistics. Springer-Verlag, New York

1981

-

[16]

Time-changed L\'evy processes and option pricing

Carr, P.\ and L.\ Wu (2004). Time-changed L\'evy processes and option pricing. Journal of Financial Economics 71(1), 113--141

2004

-

[17]

Risk Metrics and Fine Tuning of High-Frequency Trading Strategies

Cartea, \'A.\ and S.\ Jaimungal (2015). Risk Metrics and Fine Tuning of High-Frequency Trading Strategies. Mathematical Finance 25(3), 576--611. Originally circulated as a 2010 working paper

2015

-

[18]

Algorithmic and High-Frequency Trading

Cartea, \'A., S.\ Jaimungal, and J.\ Penalva (2015). Algorithmic and High-Frequency Trading. Cambridge University Press, Cambridge

2015

-

[19]

Risk Measures: Rationality and Diversification

Cerreia-Vioglio, S., F.\ Maccheroni, M.\ Marinacci, and L.\ Montrucchio (2011). Risk Measures: Rationality and Diversification. Mathematical Finance 21(4), 743--774

2011

-

[20]

A Utility Framework for Bounded-Loss Market Makers

Chen, Y.\ and D.\ M.\ Pennock (2007). A Utility Framework for Bounded-Loss Market Makers. In Proceedings of the Twenty-Third Conference on Uncertainty in Artificial Intelligence (UAI), pp.\ 49--56

2007

-

[21]

Dual characterization of properties of risk measures on Orlicz hearts

Cheridito, P.\ and T.\ Li (2008). Dual characterization of properties of risk measures on Orlicz hearts. Mathematics and Financial Economics 2(1), 29--55

2008

-

[22]

Dynamic Monetary Risk Measures for Bounded Discrete-Time Processes

Cheridito, P., F.\ Delbaen, and M.\ Kupper (2006). Dynamic Monetary Risk Measures for Bounded Discrete-Time Processes. Electronic Journal of Probability 11, 57--106

2006

-

[23]

Time-inconsistency of VaR and time-consistent alternatives

Cheridito, P.\ and M.\ Stadje (2009). Time-inconsistency of VaR and time-consistent alternatives. Finance Research Letters 6(1), 40--46

2009

-

[24]

New Measures for Performance Evaluation

Cherny, A.\ and D.\ Madan (2009). New Measures for Performance Evaluation. Review of Financial Studies 22(7), 2571--2606

2009

-

[25]

A Subordinated Stochastic Process Model with Finite Variance for Speculative Prices

Clark, P.\ K.\ (1973). A Subordinated Stochastic Process Model with Finite Variance for Speculative Prices. Econometrica 41(1), 135--155

1973

-

[26]

Representation of the penalty term of dynamic concave utilities

Delbaen, F., S.\ Peng, and E.\ Rosazza Gianin (2010). Representation of the penalty term of dynamic concave utilities. Finance and Stochastics 14(3), 449--472

2010

-

[27]

Risk Preferences and Their Robust Representation

Drapeau, S.\ and M.\ Kupper (2013). Risk Preferences and Their Robust Representation. Mathematics of Operations Research 38(1), 28--62

2013

-

[28]

Stochastic Finance: An Introduction in Discrete Time

F\"ollmer, H.\ and A.\ Schied (2016). Stochastic Finance: An Introduction in Discrete Time. Fourth edition. De Gruyter Studies in Mathematics 27. De Gruyter, Berlin

2016

-

[29]

Hedging of Contingent Claims under Incomplete Information

F\"ollmer, H.\ and M.\ Schweizer (1991). Hedging of Contingent Claims under Incomplete Information. In M.\ H.\ A.\ Davis and R.\ J.\ Elliott (Eds.), Applied Stochastic Analysis, Stochastics Monographs, Vol.\ 5, pp.\ 389--414. Gordon and Breach, New York

1991

-

[30]

The Minimal Entropy Martingale Measure and the Valuation Problem in Incomplete Markets

Frittelli, M.\ (2000). The Minimal Entropy Martingale Measure and the Valuation Problem in Incomplete Markets. Mathematical Finance 10(1), 39--52

2000

-

[31]

Maxmin expected utility with non-unique prior

Gilboa, I.\ and D.\ Schmeidler (1989). Maxmin expected utility with non-unique prior. Journal of Mathematical Economics 18(2), 141--153

1989

-

[32]

Optimal market making

Gu\'eant, O.\ (2017). Optimal market making. Applied Mathematical Finance 24(2), 112--154

2017

-

[33]

Combinatorial Information Market Design

Hanson, R.\ (2003). Combinatorial Information Market Design. Information Systems Frontiers 5(1), 107--119

2003

-

[34]

Logarithmic Market Scoring Rules for Modular Combinatorial Information Aggregation

Hanson, R.\ (2007). Logarithmic Market Scoring Rules for Modular Combinatorial Information Aggregation. Journal of Prediction Markets 1(1), 3--15

2007

-

[35]

Optimal dealer pricing under transactions and return uncertainty

Ho, T.\ and H.\ R.\ Stoll (1981). Optimal dealer pricing under transactions and return uncertainty. Journal of Financial Economics 9(1), 47--73

1981

-

[36]

Law invariant risk measures have the Fatou property

Jouini, E., W.\ Schachermayer, and N.\ Touzi (2006). Law invariant risk measures have the Fatou property. Advances in Mathematical Economics 9, 49--71

2006

-

[37]

Foundations of Modern Probability

Kallenberg, O.\ (2021). Foundations of Modern Probability. Third edition. Probability Theory and Stochastic Modelling 99. Springer, Cham

2021

-

[38]

Representation results for law invariant time consistent functions

Kupper, M.\ and W.\ Schachermayer (2009). Representation results for law invariant time consistent functions. Mathematics and Financial Economics 2(3), 189--210

2009

-

[39]

On law invariant coherent risk measures

Kusuoka, S.\ (2001). On law invariant coherent risk measures. Advances in Mathematical Economics 3, 83--95

2001

-

[40]

Market making under a weakly consistent limit order book model

Law, B.\ and F.\ Viens (2019). Market making under a weakly consistent limit order book model. High Frequency 2(3--4), 215--238

2019

-

[41]

Order-Book Modeling and Market Making Strategies

Lu, X.\ and F.\ Abergel (2018). Order-Book Modeling and Market Making Strategies. Market Microstructure and Liquidity 4(1n2), 1950003

2018

-

[42]

Ambiguity Aversion, Robustness, and the Variational Representation of Preferences

Maccheroni, F., M.\ Marinacci, and A.\ Rustichini (2006). Ambiguity Aversion, Robustness, and the Variational Representation of Preferences. Econometrica 74(6), 1447--1498

2006

-

[43]

Portfolio Selection

Markowitz, H.\ (1952). Portfolio Selection. Journal of Finance 7(1), 77--91

1952

-

[44]

Optimum consumption and portfolio rules in a continuous-time model

Merton, R.\ C.\ (1971). Optimum consumption and portfolio rules in a continuous-time model. Journal of Economic Theory 3(4), 373--413

1971

-

[45]

A Model for Queue Position Valuation in a Limit Order Book

Moallemi, C.\ C.\ and K.\ Yuan (2016). A Model for Queue Position Valuation in a Limit Order Book. Working paper, Columbia Business School Research Paper No.\ 17-70

2016

-

[46]

Risk Aversion in the Small and in the Large

Pratt, J.\ W.\ (1964). Risk Aversion in the Small and in the Large. Econometrica 32(1--2), 122--136

1964

-

[47]

Rosenbaum, M.\ and J.\ Zhang (2022). Multi-asset market making under the quadratic rough Heston. arXiv preprint arXiv:2212.10164

-

[48]

Partial Law Invariance and Risk Measures

Shen, Y., Z.\ Van Oosten, and R.\ Wang (2025). Partial Law Invariance and Risk Measures. Management Science. DOI:10.1287/mnsc.2024.06518

-

[49]

Myopia and Inconsistency in Dynamic Utility Maximization

Strotz, R.\ H.\ (1955). Myopia and Inconsistency in Dynamic Utility Maximization. Review of Economic Studies 23(3), 165--180

1955

-

[50]

Distribution-Invariant Risk Measures, Information, and Dynamic Consistency

Weber, S.\ (2006). Distribution-Invariant Risk Measures, Information, and Dynamic Consistency. Mathematical Finance 16(2), 419--441

2006

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.