The Shape of Macroeconomic Beliefs

Pith reviewed 2026-06-30 03:32 UTC · model grok-4.3

The pith

Prediction markets recover distributions of short-run inflation beliefs missed by point forecasts.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

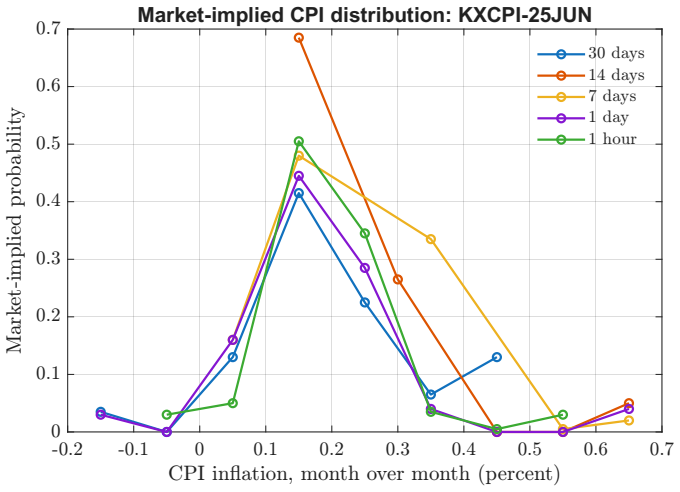

The central claim is that prediction-market prices can be turned into probability mass functions over inflation outcomes that contain real-time information about uncertainty and tail risks. Lagged Reuters Poll surprises do not shift the market mean away from consensus but do increase implied uncertainty and the probability of high inflation outcomes. In validation, the upper-tail probabilities forecast actual high-inflation episodes even when the mean is near consensus.

What carries the argument

The conversion of adjacent threshold contract prices on Kalshi into a probability mass function over possible inflation outcomes.

If this is right

- Lagged surprises increase market-implied uncertainty about inflation.

- Positive lagged surprises raise the probability assigned to high-inflation outcomes.

- Upper-tail probabilities from the market predict realizations of high inflation.

- The distributional signal provides information beyond the market mean or consensus point forecast.

Where Pith is reading between the lines

- If the approach generalizes, similar distributions could be recovered for other macroeconomic variables traded on prediction platforms.

- Policy makers could monitor these markets for early signals of shifting inflation risk.

- Extensions might test whether the same patterns hold for longer-horizon inflation expectations.

Load-bearing premise

The conversion of adjacent Kalshi threshold contract prices into a probability mass function over inflation outcomes accurately recovers the market's true belief distribution without material liquidity premia, transaction costs, or other pricing frictions.

What would settle it

A failure of the Kalshi upper-tail probabilities to predict high-inflation realizations in out-of-sample releases, particularly in cases where the implied mean matches the consensus forecast.

Figures

read the original abstract

Macroeconomic expectations are usually observed through point forecasts or through asset prices whose mapping into beliefs is model-dependent. This paper uses prediction-market prices to recover high-frequency distributions of short-run macroeconomic beliefs. We construct a panel of Kalshi-implied distributions for CPI and core CPI releases by converting adjacent threshold contracts into probability mass over inflation outcomes. The data reveal market-implied means, uncertainty, and upper-tail probabilities from 30 days to one hour before each release. The market-implied mean contains meaningful forecast information, especially for headline CPI, but the main signal is distributional. Lagged Reuters Poll surprises do not predict systematic deviations of Kalshi means from the current Reuters consensus. By contrast, large lagged surprises are associated with higher implied uncertainty, and positive lagged surprises raise the probability assigned to fixed high-inflation outcomes. In the baseline specification with variable-by-horizon fixed effects, a 0.1 percentage point positive lagged surprise raises the probability of monthly inflation above 0.3 percent by about 4.7 percentage points, even after controlling for the current consensus forecast. In release-level validation tests, Kalshi upper-tail probabilities also predict the realization of high-inflation states, including episodes in which the market-implied mean remains close to the Reuters consensus. The evidence suggests that prediction markets can provide real-time information about inflation risk that is missed by point forecasts.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper constructs high-frequency implied probability distributions for CPI and core CPI releases by converting prices of adjacent Kalshi threshold contracts into discrete probability mass functions. It reports that lagged Reuters poll surprises do not shift the market-implied mean relative to the current consensus but do increase implied uncertainty and raise the probability mass on upper-tail outcomes; in the baseline specification a 0.1 pp positive lagged surprise raises the probability of inflation above 0.3 percent by 4.7 pp after controlling for the consensus forecast. Release-level tests show these upper-tail probabilities also predict realized high-inflation states.

Significance. If the results hold, the work supplies a new source of real-time distributional beliefs about short-run macroeconomic variables that is not model-dependent in the usual sense and that appears to contain information about inflation risk missed by point forecasts. The panel structure at horizons from 30 days to one hour before release is a distinctive feature with potential value for studies of expectation updating.

major comments (2)

- [Data construction] Data construction paragraph (abstract and methods): the mapping from adjacent Kalshi threshold contract prices to a PMF over inflation bins is presented without reported checks for liquidity premia, bid-ask spreads, or inventory effects, particularly in the upper-tail contracts that define the >0.3 percent bin. Because this mapping supplies the dependent variable for the headline regression, any systematic pricing friction correlated with lagged surprises would directly affect the 4.7 pp coefficient.

- [Baseline specification] Baseline specification (results section): the regression with variable-by-horizon fixed effects reports a 4.7 pp response of P(inflation > 0.3 percent) to a 0.1 pp lagged surprise. It is not stated whether the standard errors incorporate the fact that the outcome is a generated regressor derived from noisy contract prices, nor whether the result is robust to alternative ways of allocating probability mass between adjacent thresholds.

minor comments (2)

- The abstract refers to 'release-level validation tests' but does not list the exact specifications, sample restrictions, or number of high-inflation episodes examined.

- Notation for the probability mass function and the exact thresholds used to define the upper-tail bin should be stated explicitly in the main text rather than only in the abstract.

Simulated Author's Rebuttal

We thank the referee for the constructive comments on data construction and inference. We respond to each major comment below.

read point-by-point responses

-

Referee: [Data construction] Data construction paragraph (abstract and methods): the mapping from adjacent Kalshi threshold contract prices to a PMF over inflation bins is presented without reported checks for liquidity premia, bid-ask spreads, or inventory effects, particularly in the upper-tail contracts that define the >0.3 percent bin. Because this mapping supplies the dependent variable for the headline regression, any systematic pricing friction correlated with lagged surprises would directly affect the 4.7 pp coefficient.

Authors: We agree that explicit checks for liquidity premia, bid-ask spreads, and inventory effects are warranted given that the PMF is the source of the dependent variable. The revised manuscript will add a robustness subsection that (i) reports average bid-ask spreads by horizon and contract, (ii) re-estimates the main specification using mid prices, and (iii) restricts the sample to contracts with above-median trading volume. We will also discuss the possibility of inventory effects in thin upper-tail markets and note that the headline coefficient remains stable under these checks. revision: yes

-

Referee: [Baseline specification] Baseline specification (results section): the regression with variable-by-horizon fixed effects reports a 4.7 pp response of P(inflation > 0.3 percent) to a 0.1 pp lagged surprise. It is not stated whether the standard errors incorporate the fact that the outcome is a generated regressor derived from noisy contract prices, nor whether the result is robust to alternative ways of allocating probability mass between adjacent thresholds.

Authors: We acknowledge that the outcome is a generated regressor and that the current draft does not address the resulting inference issues or alternative PMF constructions. The revision will (i) implement a bootstrap that resamples contract prices before constructing the PMFs and (ii) report the main result under two alternative mass-allocation rules (uniform within bins and linear interpolation). These additions will confirm whether the 4.7 pp coefficient and its significance are robust. revision: yes

Circularity Check

No circularity: empirical construction and regressions are externally falsifiable

full rationale

The paper performs data construction by converting adjacent Kalshi threshold contract prices into a discrete PMF over inflation bins, followed by panel regressions of implied moments and tail probabilities on lagged surprises (with controls for consensus forecasts and fixed effects). No equations, ansatzes, or uniqueness claims are present that reduce by construction to fitted inputs or prior self-citations. The PMF conversion is an identifying assumption about risk-neutral pricing, but the resulting regression coefficients are testable against realized inflation outcomes and can be replicated or falsified with independent data. No load-bearing self-citation chains or self-definitional steps appear in the provided text.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Who wins and who loses in prediction markets? Evidence from Polymarket

Akey, P., Gregoire, V., Harvie, N., Martineau, C., 2026. Who wins and who loses in prediction markets? Evidence from Polymarket. Working paper

2026

-

[2]

Fundamental disagreement

Andrade, P., Crump, R.K., Eusepi, S., Moench, E., 2016. Fundamental disagreement. Journal of Monetary Economics 83, 106--128

2016

-

[3]

The promise of prediction markets

Arrow, K.J., Forsythe, R., Gorham, M., Hahn, R., Hanson, R., Ledyard, J.O., Levmore, S., Litan, R., Milgrom, P., Nelson, F.D., Neumann, G.R., Ottaviani, M., Schelling, T.C., Shiller, R.J., Smith, V.L., Snowberg, E., Sunstein, C.R., Tetlock, P.C., Tetlock, P.E., Varian, H.R., Wolfers, J., Zitzewitz, E., 2008. The promise of prediction markets. Science 320,...

2008

-

[4]

A model of investor sentiment

Barberis, N., Shleifer, A., Vishny, R., 1998. A model of investor sentiment. Journal of Financial Economics 49, 307--343

1998

-

[5]

Prediction market accuracy in the long run

Berg, J.E., Nelson, F.D., Rietz, T.A., 2008. Prediction market accuracy in the long run. International Journal of Forecasting 24, 285--300

2008

-

[6]

Diagnostic expectations and stock returns

Bordalo, P., Gennaioli, N., La Porta, R., Shleifer, A., 2019. Diagnostic expectations and stock returns. Journal of Finance 74, 2839--2874

2019

-

[7]

Salience theory of choice under risk

Bordalo, P., Gennaioli, N., Shleifer, A., 2012. Salience theory of choice under risk. Quarterly Journal of Economics 127, 1243--1285

2012

-

[8]

Diagnostic expectations and credit cycles

Bordalo, P., Gennaioli, N., Shleifer, A., 2018. Diagnostic expectations and credit cycles. Journal of Finance 73, 199--227

2018

-

[9]

Makers and takers: The economics of the Kalshi prediction market

Burgi, C., Deng, W., Whelan, K., 2026. Makers and takers: The economics of the Kalshi prediction market. Working Paper 2026-001, George Washington University, Center for Economic Research

2026

-

[10]

Macroeconomic expectations of households and professional forecasters

Carroll, C.D., 2003. Macroeconomic expectations of households and professional forecasters. Quarterly Journal of Economics 118, 269--298

2003

-

[11]

Prediction markets? The accuracy and efficiency of \ 2.4 billion in the 2024 presidential election

Clinton, J.D., Huang, T., 2025. Prediction markets? The accuracy and efficiency of \ 2.4 billion in the 2024 presidential election. SocArXiv preprint

2025

-

[12]

What can survey forecasts tell us about information rigidities? Journal of Political Economy 120, 116--159

Coibion, O., Gorodnichenko, Y., 2012. What can survey forecasts tell us about information rigidities? Journal of Political Economy 120, 116--159

2012

-

[13]

Information rigidity and the expectations formation process: A simple framework and new facts

Coibion, O., Gorodnichenko, Y., 2015. Information rigidity and the expectations formation process: A simple framework and new facts. American Economic Review 105, 2644--2678

2015

-

[14]

Introducing: The Survey of Professional Forecasters

Croushore, D., 1993. Introducing: The Survey of Professional Forecasters. Business Review, Federal Reserve Bank of Philadelphia, 3--15

1993

-

[15]

Investor psychology and security market under- and overreactions

Daniel, K., Hirshleifer, D., Subrahmanyam, A., 1998. Investor psychology and security market under- and overreactions. Journal of Finance 53, 1839--1885

1998

-

[16]

Kalshi and the rise of macro markets

Diercks, A.M., Katz, J.D., Wright, J.H., 2026. Kalshi and the rise of macro markets. NBER Working Paper 34702

2026

-

[17]

The anatomy of a decentralized prediction market: Microstructure evidence from the Polymarket order book

Dubach, P.D., 2026. The anatomy of a decentralized prediction market: Microstructure evidence from the Polymarket order book. Working paper

2026

-

[18]

Prediction markets underperform simple baselines for infectious disease forecasting

Dudley, C., Magdaleno, R., 2026. Prediction markets underperform simple baselines for infectious disease forecasting. Working paper

2026

-

[19]

Under pressure? Central bank independence meets blockchain prediction markets

Eichengreen, B., Viswanath-Natraj, G., Wang, J., Wang, Z., 2025. Under pressure? Central bank independence meets blockchain prediction markets. SSRN Working Paper

2025

-

[20]

Comparing the point predictions and subjective probability distributions of professional forecasters

Engelberg, J., Manski, C.F., Williams, J., 2009. Comparing the point predictions and subjective probability distributions of professional forecasters. Journal of Business & Economic Statistics 27, 30--41

2009

-

[21]

Anatomy of an experimental political stock market

Forsythe, R., Nelson, F., Neumann, G.R., Wright, J., 1992. Anatomy of an experimental political stock market. American Economic Review 82, 1142--1161

1992

-

[22]

Financial prediction markets: A new measure of earnings expectations

Gomez-Cram, R., Guo, Y., Jensen, T.I., Kung, H., 2025. Financial prediction markets: A new measure of earnings expectations. Working paper

2025

-

[23]

Prediction market accuracy: Crowd wisdom or informed minority? Working paper

Gomez-Cram, R., Guo, Y., Jensen, T.I., Kung, H., 2026. Prediction market accuracy: Crowd wisdom or informed minority? Working paper

2026

-

[24]

A unified theory of underreaction, momentum trading, and overreaction in asset markets

Hong, H., Stein, J.C., 1999. A unified theory of underreaction, momentum trading, and overreaction in asset markets. Journal of Finance 54, 2143--2184

1999

-

[25]

Expectations and the neutrality of money

Lucas, R.E., 1972. Expectations and the neutrality of money. Journal of Economic Theory 4, 103--124

1972

-

[26]

Sticky information versus sticky prices: A proposal to replace the New Keynesian Phillips curve

Mankiw, N.G., Reis, R., 2002. Sticky information versus sticky prices: A proposal to replace the New Keynesian Phillips curve. Quarterly Journal of Economics 117, 1295--1328

2002

-

[27]

Interpreting the predictions of prediction markets

Manski, C.F., 2006. Interpreting the predictions of prediction markets. Economics Letters 91, 425--429

2006

-

[28]

From Iran to Taylor Swift: Informed trading in prediction markets

Mitts, J., Ofir, M., 2026. From Iran to Taylor Swift: Informed trading in prediction markets. Working paper

2026

-

[29]

Social value of public information

Morris, S., Shin, H.S., 2002. Social value of public information. American Economic Review 92, 1521--1534

2002

-

[30]

Rational expectations and the theory of price movements

Muth, J.F., 1961. Rational expectations and the theory of price movements. Econometrica 29, 315--335

1961

-

[31]

Beating the earnings game: Why do prediction markets outperform professional analysts? SSRN Working Paper

Rabetti, D., Shao, J., Zhang, C., 2026. Beating the earnings game: Why do prediction markets outperform professional analysts? SSRN Working Paper

2026

-

[32]

Unravelling the probabilistic forest: Arbitrage in prediction markets

Saguillo, O., Ghafouri, V., Kiffer, L., Suarez-Tangil, G., 2025. Unravelling the probabilistic forest: Arbitrage in prediction markets. Working paper

2025

-

[33]

Implications of rational inattention

Sims, C.A., 2003. Implications of rational inattention. Journal of Monetary Economics 50, 665--690

2003

-

[34]

Prediction markets for economic forecasting

Snowberg, E., Wolfers, J., Zitzewitz, E., 2013. Prediction markets for economic forecasting. In: Elliott, G., Timmermann, A. (Eds.), Handbook of Economic Forecasting, vol. 2. Elsevier, Amsterdam, pp. 657--687

2013

-

[35]

The effects of monetary policy on macroeconomic expectations: High-frequency evidence from prediction markets

Swanson, E.T., Wang, R., Wu, Y., 2025. The effects of monetary policy on macroeconomic expectations: High-frequency evidence from prediction markets. Manuscript

2025

-

[36]

The anatomy of a blockchain prediction market: Polymarket in the 2024 U.S

Tsang, K.P., Yang, Z., 2026a. The anatomy of a blockchain prediction market: Polymarket in the 2024 U.S. presidential election. Working paper

2024

-

[37]

Political shocks and price discovery: Evidence from Polymarket during the 2024 U.S

Tsang, K.P., Yang, Z., 2026b. Political shocks and price discovery: Evidence from Polymarket during the 2024 U.S. presidential election. Working paper

2024

-

[38]

Prediction markets

Wolfers, J., Zitzewitz, E., 2004. Prediction markets. Journal of Economic Perspectives 18, 107--126

2004

-

[39]

Interpreting prediction market prices as probabilities

Wolfers, J., Zitzewitz, E., 2006. Interpreting prediction market prices as probabilities. NBER Working Paper 12200

2006

-

[40]

Imperfect common knowledge and the effects of monetary policy

Woodford, M., 2003. Imperfect common knowledge and the effects of monetary policy. In: Aghion, P., Frydman, R., Stiglitz, J.E., Woodford, M. (Eds.), Knowledge, Information, and Expectations in Modern Macroeconomics: In Honor of Edmund S. Phelps. Princeton University Press, Princeton, pp. 25--58

2003

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.