Quality-Adjusted Hit-Ratio Targeting in Corporate Bond Market Making

Pith reviewed 2026-06-28 23:19 UTC · model grok-4.3

The pith

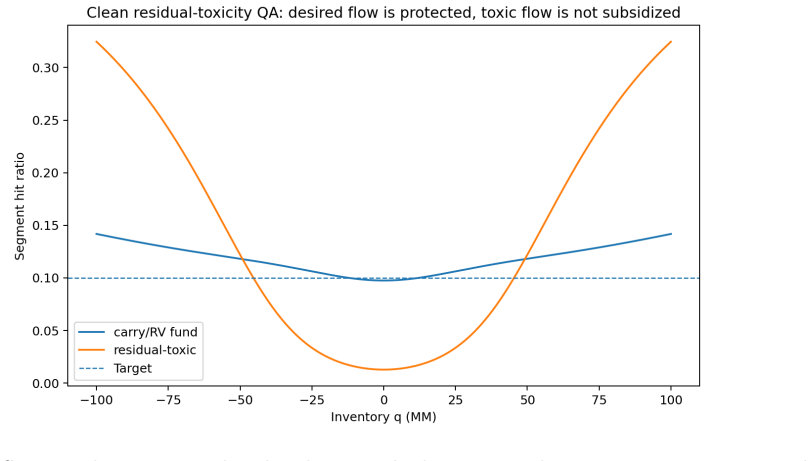

Replacing raw hit-ratio targets with a residual-quality-adjusted version reallocates corporate bond market-making service away from high-toxicity client flow.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The central claim is that a residual-quality-adjusted hit ratio, formed by first removing observable credit, carry, relative-value, and demand effects from post-trade markouts and penalizing only the remaining adverse-selection component, produces a tractable control problem whose solution reallocates quoting service away from residual-toxic flow. Under the quadratic approximation the optimal quote decomposes into riskless spread, inventory skew, credit-alpha skew, residual-toxicity charge, and quality-hit-ratio subsidy; the dual variable for each targeted tier solves an exact one-dimensional nonlinear fixed point. Multi-bond simulations with nonlinear dual solves show that raw hit-ratio con

What carries the argument

Residual-quality-adjusted hit ratio obtained by decomposing adverse markouts into observable factors and penalizing only the residual adverse-selection component inside the stochastic-control penalty.

If this is right

- Optimal quotes explicitly include a residual-toxicity charge and a quality-hit-ratio subsidy in addition to riskless spread, inventory skew, and credit-alpha skew.

- Raw hit-ratio targets can subsidize residual-toxic flow while quality-adjusted targets reallocate service toward low-residual-toxicity clients.

- The dual variable for each hit-ratio tier solves a one-dimensional nonlinear fixed-point equation, keeping the HJB separable.

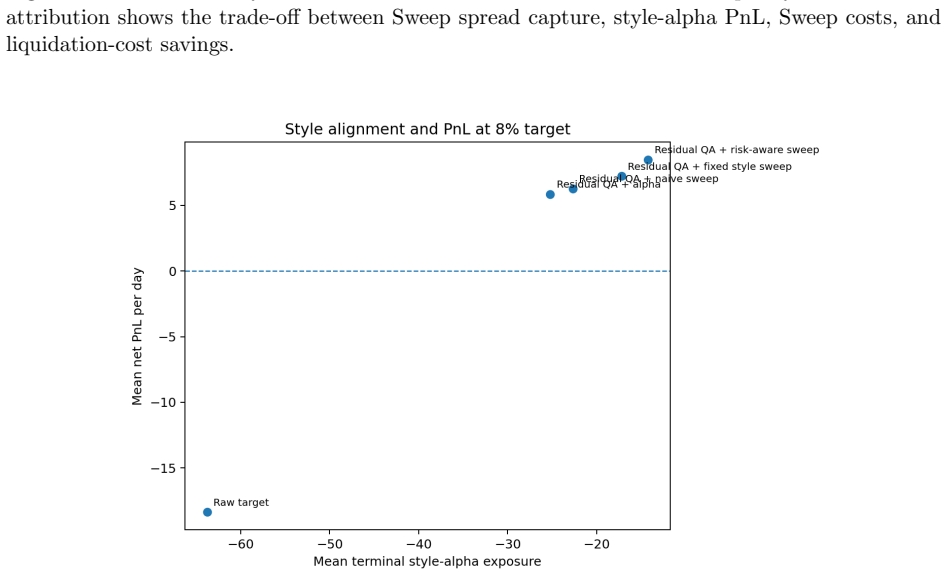

- Inventory-recycling value through risk-aware style-aligned warehousing of sweep or portfolio trades can be sized with the same quadratic approximation used for RFQ quoting.

- Forecastable passive or index-demand flow is handled as a special case of the same control problem.

Where Pith is reading between the lines

- The decomposition approach could be tested on other OTC asset classes where post-trade markouts contain both observable and residual components.

- Relaxing the quadratic value-function approximation would allow direct numerical solution of the HJB to quantify approximation error in the optimal quotes.

- Portfolio-trade participation rules derived from the warehousing extension could interact with the quality-adjusted hit-ratio constraint when multiple bonds are quoted simultaneously.

- If the residual component proves stable across market regimes, the same fixed-point dual solve could be embedded in real-time quoting engines without proprietary data.

Load-bearing premise

Adverse post-trade markouts can be decomposed accurately enough that the leftover residual component truly isolates client-flow toxicity rather than omitted observable effects.

What would settle it

Live RFQ data in which the residual component after the stated decomposition shows no out-of-sample predictive power for subsequent adverse markouts, or in which the quality-adjusted quotes fail to improve realized profitability per unit of hit ratio relative to raw targeting.

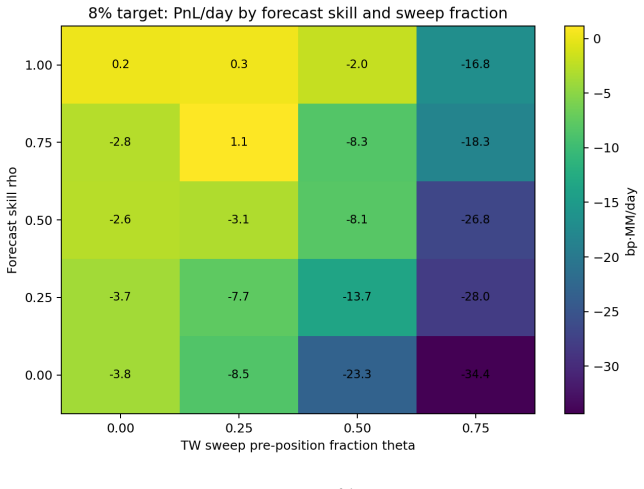

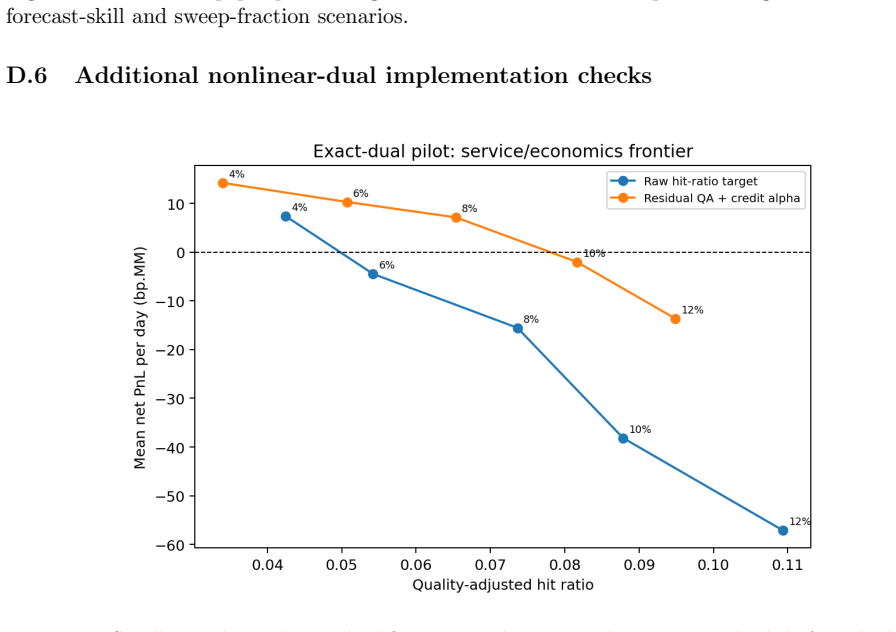

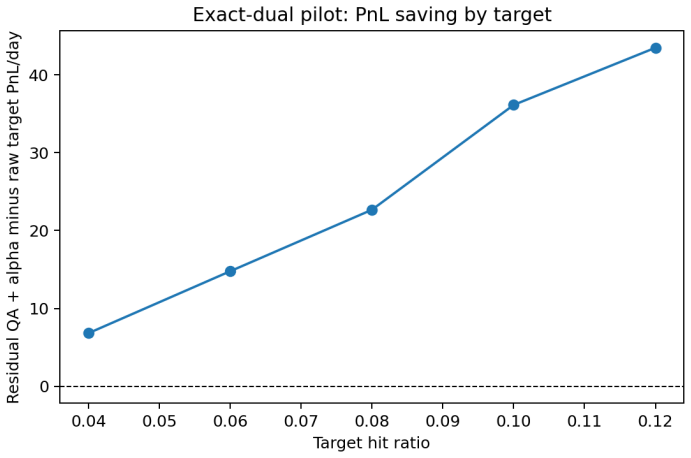

Figures

read the original abstract

Hit ratio is a common service metric for electronic corporate bond market making, but raw hit-ratio targets can be economically misleading when client flow has heterogeneous adverse-selection content. This paper extends a stochastic-control framework for OTC bond RFQ market making with hit-ratio constraints by replacing raw hit ratio with a residual-quality-adjusted hit ratio. The key modelling distinction is that adverse post-trade markouts are first decomposed into observable credit factors, carry/rolldown, issuer-relative-value effects, index or ETF demand effects, and residual adverse selection. Only the residual component is treated as client-flow toxicity. The resulting control problem remains tractable: after dualizing the quality-hit-ratio penalty, the HJB retains separable Hamiltonians, and the dual variable is the solution of an exact one-dimensional nonlinear fixed point for each targeted tier. Under a quadratic value-function approximation, optimal quotes decompose into a riskless spread, inventory skew, credit-alpha skew, residual-toxicity charge, and quality-hit-ratio subsidy. Synthetic multi-bond simulations with nonlinear dual solves illustrate that raw hit-ratio targeting can subsidize residual-toxic flow, while residual-quality targeting reallocates service toward low-residual-toxicity flow and improves the attained service/economics frontier. A final reduced-form extension studies inventory-recycling value through risk-aware style-aligned client-flow warehousing. Sweep or portfolio-trade opportunities fill randomly, and participation is sized using the same quadratic value approximation as the RFQ quoting problem. A passive/index-demand experiment is reported in the appendix as a special case of forecastable client flow. The numerical evidence is synthetic and mechanism-oriented; no proprietary RFQ data are used.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper extends a stochastic-control model for OTC corporate-bond RFQ market making by replacing a raw hit-ratio constraint with a residual-quality-adjusted hit ratio. Adverse post-trade markouts are decomposed into observable components (credit factors, carry/rolldown, issuer RV, index/ETF demand) plus a residual adverse-selection term that alone is treated as client-flow toxicity. After dualization the HJB remains separable; the dual variable solves a one-dimensional nonlinear fixed point per tier. Under a quadratic value-function approximation the optimal quotes decompose into riskless spread, inventory skew, credit-alpha skew, residual-toxicity charge and quality-hit-ratio subsidy. Synthetic multi-bond simulations with nonlinear dual solves are used to illustrate that raw hit-ratio targeting subsidizes residual-toxic flow while the quality-adjusted version reallocates service toward low-residual-toxicity counterparties and improves the service/economics frontier. A reduced-form inventory-recycling extension and a passive/index-demand appendix case are also presented. All evidence is synthetic; no proprietary RFQ data appear.

Significance. If the clean decomposition of markouts into observables versus residual toxicity can be maintained in live trading, the framework supplies a tractable way to enforce service metrics without inadvertently subsidizing toxic flow. The dual fixed-point construction and quadratic approximation preserve separability, which is a technical strength for implementation. However, because the reported frontier improvement is demonstrated only under perfect synthetic decomposition and no real-market validation or perturbation analysis is supplied, the practical significance remains illustrative rather than immediately actionable for market-making desks.

major comments (2)

- [Synthetic multi-bond simulations] The central claim that residual-quality targeting 'reallocates service toward low-residual-toxicity flow and improves the attained service/economics frontier' is demonstrated exclusively in synthetic multi-bond simulations where the markout decomposition is exact by construction. No perturbation analysis (noisy factor estimates, omitted variables, or residual contamination) is reported to show whether the HJB-derived quotes or the one-dimensional nonlinear fixed-point dual still deliver the claimed improvement when the residual is imperfectly observed. This assumption is load-bearing for the modeling distinction stated in the abstract.

- [Abstract / dualization paragraph] The abstract states that the dual variable 'is the solution of an exact one-dimensional nonlinear fixed point for each targeted tier,' yet the manuscript supplies neither the explicit fixed-point equation nor an error analysis or convergence proof for the nonlinear solve. Without these derivations it is impossible to assess whether the fixed point remains independent of the target result or reduces to a fitted quantity, undermining the claim of tractability after dualization.

minor comments (1)

- The quadratic value-function approximation is listed among the free parameters; its functional form and calibration procedure should be stated explicitly in the main text rather than left implicit.

Simulated Author's Rebuttal

We thank the referee for the constructive comments. The feedback correctly identifies that the current evidence is limited to exact synthetic decompositions and that the dual fixed-point construction requires more explicit derivation. We address each point below and will incorporate the suggested additions in revision.

read point-by-point responses

-

Referee: [Synthetic multi-bond simulations] The central claim that residual-quality targeting 'reallocates service toward low-residual-toxicity flow and improves the attained service/economics frontier' is demonstrated exclusively in synthetic multi-bond simulations where the markout decomposition is exact by construction. No perturbation analysis (noisy factor estimates, omitted variables, or residual contamination) is reported to show whether the HJB-derived quotes or the one-dimensional nonlinear fixed-point dual still deliver the claimed improvement when the residual is imperfectly observed. This assumption is load-bearing for the modeling distinction stated in the abstract.

Authors: We agree that the simulations assume exact decomposition by construction, which isolates the mechanism but leaves open the question of robustness. In the revision we will add a new subsection containing perturbation experiments: Gaussian noise will be added to the observable markout components, omitted-variable scenarios will be simulated, and residual contamination will be introduced. The HJB quotes and the nonlinear dual fixed-point solves will be re-computed under these conditions to test whether the reported service/economics frontier improvement is preserved. This directly addresses the load-bearing assumption. revision: yes

-

Referee: [Abstract / dualization paragraph] The abstract states that the dual variable 'is the solution of an exact one-dimensional nonlinear fixed point for each targeted tier,' yet the manuscript supplies neither the explicit fixed-point equation nor an error analysis or convergence proof for the nonlinear solve. Without these derivations it is impossible to assess whether the fixed point remains independent of the target result or reduces to a fitted quantity, undermining the claim of tractability after dualization.

Authors: We acknowledge that the explicit fixed-point equation and convergence details are not supplied in the current text. The revision will add an appendix that (i) derives the one-dimensional nonlinear fixed-point equation obtained after dualization of the quality-adjusted hit-ratio constraint, (ii) states the precise mapping from the dual variable to the target tier, and (iii) reports numerical convergence diagnostics (iteration counts and residual norms) for a range of target values. This will allow readers to verify independence from the target and confirm tractability. revision: yes

Circularity Check

Synthetic simulations demonstrate reallocation benefit under exact decomposition by construction

specific steps

-

fitted input called prediction

[Abstract]

"Synthetic multi-bond simulations with nonlinear dual solves illustrate that raw hit-ratio targeting can subsidize residual-toxic flow, while residual-quality targeting reallocates service toward low-residual-toxicity flow and improves the attained service/economics frontier."

The synthetic data is generated from the same credit factors, carry/rolldown, issuer-relative-value, and index/ETF demand components used to decompose markouts and isolate the residual toxicity term. The claimed improvement therefore obtains by construction whenever the decomposition is exact, without independent falsification.

full rationale

The paper's central claim—that residual-quality-adjusted hit-ratio targeting improves the service/economics frontier relative to raw hit-ratio targeting—is illustrated exclusively via synthetic multi-bond simulations. These simulations generate markout data from the identical observable factors (credit, carry/rolldown, issuer RV, index/ETF demand) used to define the decomposition, with only the residual labeled toxicity. Consequently the reported reallocation and frontier improvement hold exactly when the decomposition is perfect, which is the modeling assumption itself. The HJB separability and one-dimensional dual fixed-point solve are presented as independent, but the validation step reduces to the input construction. No perturbation, omitted-variable, or noisy-estimate analysis is described, producing partial circularity confined to the numerical evidence.

Axiom & Free-Parameter Ledger

free parameters (1)

- quadratic value-function approximation

axioms (1)

- domain assumption Adverse post-trade markouts can be decomposed into observable factors plus residual toxicity

Reference graph

Works this paper leans on

-

[1]

and Stoikov, S

Avellaneda, M. and Stoikov, S. (2008). High-frequency trading in a limit order book.Quanti- tative Finance, 8(3), 217–224

2008

-

[2]

Gueant, O., Lehalle, C.-A., and Fernandez-Tapia, J. (2013). Dealing with the inventory risk: a solution to the market making problem.Mathematics and Financial Economics, 7, 477–507

2013

-

[3]

and Manziuk, I

Gueant, O. and Manziuk, I. (2019). Deep reinforcement learning for market making in corporate bonds: beating the curse of dimensionality.Applied Mathematical Finance, 26(5), 387–452

2019

-

[4]

Bond Market Making with a Hit-Ratio Target

Barzykin, A. and Ciceri, A. (2026). Bond Market Making with a Hit-Ratio Target. arXiv:2604.20406. 37

work page internal anchor Pith review Pith/arXiv arXiv 2026

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.